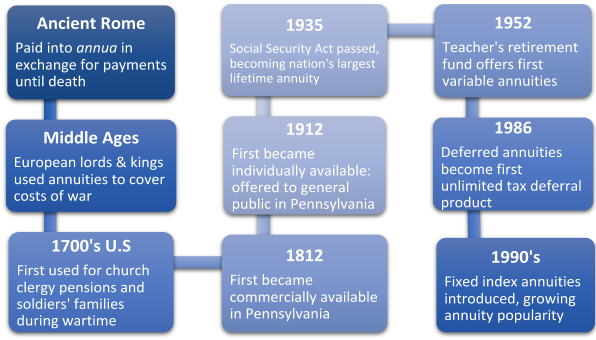

Welcome back to our series about annuities! This time, we will be diving a little deeper into the basics of annuities. We will look at how annuities work and some important terms to concentrate on when thinking about an annuity or examining an annuity contract. First, let’s take a look at the history of annuities. They’ve been around for a very long time and have evolved over the many years.