![]()

Social Security plays a major role in cash flow for retirees and we will help you understand how the benefits work and what you should do before you start claiming Social Security. A married couple could have over 70+ different ways to claim Social Security! In order to maximize a major cash flow for your retirement it is key to understand your options. This checklist will help you ensure that you are maximizing your benefits and will help lower stress levels going into this decision.

1. Know the exact age and dollar amount you will receive.

Any person can visit www.SSA.gov/myaccount and log in/create an account to view their benefits. You will see your yearly earnings and a summary chart that will break down early retirement, full retirement age, or late retirement. These breakdowns will show the monthly dollar amount you are eligible to receive. The website has an interactive tracker that lets you see benefits at different ages. For those who are several years out until retirement, you can estimate your future earnings and see how this affects your monthly amount.

Benefits are calculated using changing variables over an individual’s life, including the number of years worked, average annual earnings, and retirement age. Since these values are always changing, it is a good idea to log in and create an account to have a general idea of their benefit amount.

2. The right time to claim benefits is different for everyone and dependent on their situation.

Determining the right time to claim benefits is usually the number one hang-up for everyone going into retirement. This is a decision that requires a little bit of math and art. Nobody knows the day they will pass away and by starting their benefits too early, you could end up with less income during your later years than you need. By starting your benefits too late, you run the risk of spending other retirement assets or passing away before you have the chance to take what you’ve earned.

Every eligible American can start receiving social security at age 62, by claiming any age earlier than the full retirement age, you will receive a discounted monthly amount. The longer you wait, the more you will earn and 70 is the latest age to claim maximum benefit.

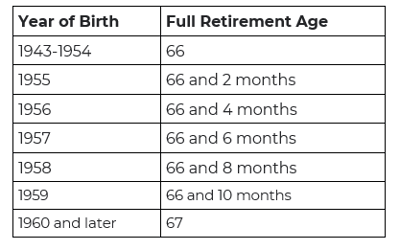

Full retirement age is based on your year of birth:

There is not a one size fits all strategy to start claiming benefits and one person may benefit from starting to take Social Security at 62 and the other may benefit at age 70. Talking with the team at Creekmur Wealth will help ease the decision with facts instead of emotions. Ultimately it is an individual’s choice of age to start claiming, but a second opinion may help guide your decision.

3. Social Security benefits could increase your taxable income.

People may opt to claim Social Security while still working. However, if they’re under full retirement age, benefits will be subject to the earnings test and could be reduced by $1 for every $2 over the earnings limit. (The earnings limit is $21,240 in 2023). Then in the year you reach full retirement age, your benefits are reduced by $1 for every $3 in income over $56,520. This will continue until you reach full retirement age. Keep in mind that your decreased earnings are not gone forever. Social Security will credit it to your record when you reach full retirement age, which equals a higher benefit.

4. You may be eligible for spousal benefits.

Spending time out of the workforce for whatever reason may not make you eligible to receive Social Security, but if your spouse has worked and can receive Social Security, you may be eligible for spousal benefits. Nonworking spouses can qualify for a portion of their partner's benefits as long as the working spouse has already started receiving benefits and they are at or over the age of 62.

Like traditional benefits, spousal benefits are reduced if the non-working spouse begins to take Social Security before the full retirement age. Spousal benefits also stop growing after the nonworking spouse reaches their full retirement age and they can receive up to 50% of their partner’s full benefit.

5. Your spouse may be able to take over benefits when you pass away.

If you are married at the time of your death, the surviving spouse becomes eligible to take your benefits once they reach age 60, or at 50 if they are disabled. The surviving spouse can decide whether to keep their own benefits or take over their spouse's benefits (if higher). The benefits will be reduced if the surviving spouse hasn’t reached full retirement age. The earnings test will apply if the surviving spouse is still working. If the surviving spouse remarries prior to age 60, they will not be eligible.

6. Spousal benefits may apply even if you’re divorced.

Certain criteria need to be met if you want to claim your spouse's benefit after a divorce.

-

- Marriage had to last 10 years.

- You have not been remarried.

- You (and your former spouse) have reached age 62.

- You aren’t eligible for higher benefits on your own

If this criterion has been met, you may be eligible for 50% of your former spouse's full benefits.

7. You can change your mind one time but have limited time to do so.

Once you have made the decision to start benefits, you can actually make a change to pause your benefits. Social Security lets you withdraw your application for benefits one time in the 12 months after you start claiming. Of course, you will have to pay the full amount received back to Social Security and will receive a credit to your future benefits. By continuing to hold off on claiming your benefits for a few years you will increase your monthly benefit amount in the future.

People typically do not know this is an option and it happens a lot when someone retires and immediately starts to claim benefits. They find themselves going back to work for one reason or another, and do not need income from Social Security. In this situation, it may make sense to halt benefits and repay the income to hold out for higher monthly checks.

Final Observations

When is the best time to start taking benefits? That decision will depend entirely on your personal situation and consulting with the team at Creekmur Wealth will help take emotion out of the decision. This is a huge income source for all retirees and having a rock-solid financial plan and income plan is necessary for a stress-free retirement. If you are heading down the road of retirement and would like to go over your options or want a second opinion, please call us to set up a time to speak.

Best Regards,

Andrew Pisel

Wealth Advisor

Sources

1. Social Security Administration. “Starting Your Retirement Benefits Early.” https://www.ssa.gov/benefits/retirement/planner/agereduction.html. Accessed Feb. 13, 2023.

2. Social Security Administration. “Receiving Benefits While Working.” https://www.ssa.gov/benefits/retirement/planner/whileworking.html. Accessed Feb. 13, 2023.

3. Social Security Administration. “Benefits for Spouses.” https://www.ssa.gov/oact/quickcalc/spouse.html. Accessed Feb. 13, 2023.

4. Social Security Administration. “If You Are the Survivor.” https://www.ssa.gov/benefits/survivors/ifyou.html. Accessed Feb. 13, 2023.

5. Social Security Administration. “Benefits For Your Family.” https://www.ssa.gov/benefits/retirement/planner/applying7.html#h4. Accessed Feb. 13, 2023.

6. AARP. Dec. 23, 2022. “Can I stop Social Security benefits and restart them later to get a bigger payment?” https://www.aarp.org/retirement/social-security/questions-answers/social-security-going-back-to-work.html. Accessed Feb. 13, 2023.

7. https://aewealthmanagement.com/blog/aewm-wealth-report-7-things-to-know-about-social-security-before-starting-benefits/