You've spent years planning for retirement. But now you're wondering if your retirement dollars will last through the ups and downs of the stock market.

The good news is that we have a plan for that.

Sometimes in life the order in which events occur matters. For instance, would you rather jump in the ocean and then learn to swim? Or is it better to learn to swim and then jump in the ocean? One of those scenarios would likely have a better outcome than the other, and it’s due to the sequence of those two events.

Believe it or not, your retirement portfolio is subject to a similar sequencing risk known as the sequence of returns. Sequence of returns refers to the order in which a portfolio’s returns occur (either negative or positive). Similar to jumping into an ocean without knowing how to swim, failing to prepare for a poor sequence of returns in retirement could be the difference between sinking or swimming.

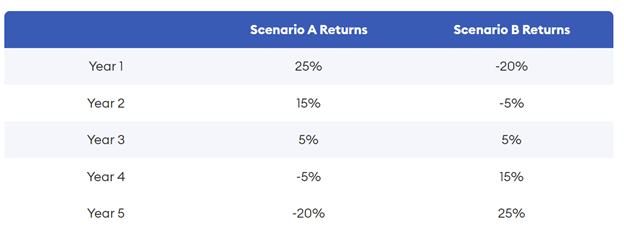

Forbes published an article regarding the impact of good versus bad sequence of return. The article showed the impact of opposite returns over a 5 year period as shown below. You can see that the total return over those 5 years are exactly identical - just in reverse order.

In either scenario a $100,000 investment would yield the same result after five years, $114,712.50 compounded annually. However, things can look very differently if an investor were taking distributions during this time frame.

👉Watch 5 Minute Finances: Why Sequence of Returns Matter

Imagine that a retiree were to withdraw $10,000 per year from their $100,000 portfolio during this hypothetical time period. The sequence of returns would cause very different outcomes after 5 years:

Scenario A - our portfolio would be more than $70,000 after five years, with a CAGR (compound adjusted growth rate) of -4.77%.

Scenario B - our portfolio would be worth just under $47,000 after five years, with a CAGR of -12.21%.

Cleary, this level of variability can have a big impact on your retirement portfolio.

So, how can a retiree can plan for this?

Luckily, retirement is more than just a coin flip to see what sequence you end up with. There are strategies that can be employed to reduce the impact of a poor sequence of returns.

One such strategy is our “bucket strategy.” This is a portfolio strategy that involves matching investment risk to time frames. We break up the portfolio into three different time frames—dollars that will be used in the short term (0-3 years), intermediate term (4-6 years), and long term (7+ years).

For dollars falling into the short term bucket, sequence of returns is much more important as there is little time for these short term dollars to recover from a drop in value. As such, we significantly reduce the stock market risk by utilizing annuities, investments with lower volatility, or even cash options such as CDs or savings accounts.

In the intermediate term bucket, since there is more time between now and withdrawal, the level of risk can be increased since a short term drop in value now has more time to recover. By increasing risk we expect a higher return in exchange for more volatility. Investments in this bucket have traditionally included fixed income investments or low risk stocks such as dividend paying stocks.

Finally, in the long term bucket we have dollars that will not be accessed for many years. A drop in value of ten, twenty, or even thirty percent in the short term is of less concern because we do not need to access these dollars for years or even decades. As such we can leave them invested for growth. In exchange for the higher risk we would expect a much higher rate of return over the long term. The investments in this bucket would be more growth oriented stocks or funds. This is the bucket that will provide the growth necessary to fund your future spending needs and combat the impact of inflation over time.

Just as a contractor can use the same hammer to build many unique homes, as investment advisors we may use the same tool for many of our clients. The “bucket strategy” may be one of our hammers, but we can use it to create a plan that is fully customized to meet your specific retirement goals.

Andy

Do you have other questions about retirement?

Text our team for answers at 309-925-2043!