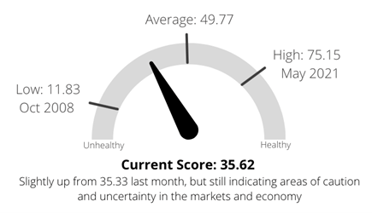

Market Health Indicator

The Market Health Indicator (MHI) measures market health on a scale of 0 - 100, analyzing various market segments such as economics, technicals, and volatility. Higher scores indicate healthier market conditions.

October was filled with more tricks than treats as markets continued to slump.

Rising interest rates, combined with heightened geopolitical uncertainties, weighed on market sentiment. While there was no Fed meeting during the month, investors priced in higher rates for longer. Some stronger-than-expected economic data supported this viewpoint as the labor market added more jobs than forecast, consumer spending remained relatively strong, and GDP showed the US economy expanded more than predicted.

Small-cap stocks were the laggards again, realizing further downside pressure as the Russell 2000 fell 6.88%. The larger US indices held up better but still finished the month negative with losses of 1.36%, 2.20%, and 2.78% for the Dow Jones Industrial Average, S&P 500, and Nasdaq respectively. It was the third consecutive negative month for broad equity markets, marking the longest monthly losing streak since early 2020.

Stocks overseas also slipped lower, lagging their US counterparts as developed international stocks dropped 3.39% and emerging markets lost 3.24%. The rising tensions in Israel, in addition to the ongoing Russia - Ukraine conflict, further dampened global risk appetite.

There was no Fed meeting in October, but interest rates continued to climb on the expectation of rates being held higher for longer. The 10-year Treasury yield rose from 4.59% to 4.88%, resulting in a loss of 1.37% for the aggregate US bond market. This marks the sixth consecutive monthly decline for traditional bonds as rising rates have remained a headwind. However, the silver lining is once they level off higher rates will eventually be a positive for bonds, providing higher income payments for the future. Despite the recent downward pressure, this is already becoming apparent as aggregate US bonds are down only 1.77% YTD, compared to a loss of 13.02% in 2022.

While each year is unique, the last couple of months of the year tend to be seasonally strong, and investors are hoping this holds true as we enter the holiday season. Market volatility and uncertainty can be understandably disconcerting, but having an appropriate plan in place can help block out the short-term noise and keep focus on reaching the more important longer-term goals.

Story 1

What do tires, stars, and hotels have in common? The Michelin Man.

The French tire company started the Michelin Guide in 1900 to help travelers plan their long-distance trips (so it could sell more tires).

After 123 years of recommending restaurants, with its first stars being awarded in 1926, the Michelin Guide is jumping into the hotel space.

Similar to its famous star rating system, Michelin will grant “keys” to hotels from around the world that meet its high standards, relying on its own judges who will anonymously check into rooms.

Judges will consider five factors when it comes to rating the hotels - destination locations, architecture and interior design, service, unique character, and value.

The move comes as more companies look to grab a bigger piece of the growing travel and hospitality industry amid strong demand.

Story 2

It’s being dubbed Pharmageddon, not to be confused with the 1998 film starring Bruce Willis.

Pharmacists at multiple chains across the US, including CVS and Walgreens, have organized walkouts as recent protests have gained momentum.

However, unlike the auto industry and writers guild strikes, pharmacy workers aren’t demanding bigger paychecks.

Instead, the pharmacists are asking their employers to hire more staff and change policies that are causing them to rush filling prescriptions.

Nearly three-quarters of pharmacists surveyed said they didn’t have enough time to safely do their jobs, which was exacerbated with the pandemic as new vaccines became available.

Major pharmacy chains have plans to close 1.5k stores in an effort to cut costs, which could accelerate the adoption of mail-order services.

The information presented is not investment advice - it is for educational purposes only and is not an offer or solicitation for the sale or purchase of any securities or investment advisory services. Investments involve risk and are not guaranteed. Be sure to consult with a qualified financial adviser when making investment decisions.