Why is the Stock Market increasing in the midst of such uncertainty?

This year has been quite the ride in markets both domestic and global. Here in the U.S. we have experienced the quickest slide into a bear market in history, followed by an equally incredible market bounce in short order:

The burning question that has been asked routinely by clients, journalists, market prognosticators, and our firm is WHY this bounce occurred in the face of such dire economic expectations. There are numerous economic and market factors that we will consider in future days, but today let's focus on a topic that has an important impact on market performance: The construction of the S&P 500 and the role that plays in this market recovery.

The S&P 500 is comprised of the 500 largest companies in the United States. The index is calculated using the “free-float market capitalization weighted methodology”. Simply stated, the index is calculated by dividing the market capitalization of an individual stock by the total market capitalization of all 500 companies included in the S&P 500.

Since the S&P 500 is based on the market capitalization method, the companies who are the largest in terms of market capitalization will have an out sized impact on the overall returns of the index. Currently the top 10 holdings in the S&P 500 comprise 26.50% of the total index, these companies are:1

|

Microsoft Corp. |

JP Morgan Chase & Co. |

|

Apple Inc. |

Proctor Gamble & Co. |

|

Amazon.com Inc. |

Visa Inc. |

|

Alphabet Inc. |

Johnson & Johnson |

|

Facebook Inc. |

Berkshire Hathaway Inc. |

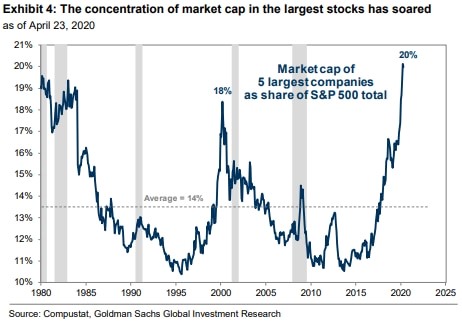

While it is not incredibly abnormal for the top 10 companies to comprise roughly a quarter of the S&P 500 index, it is abnormal for the top 5 companies to comprise 20% of the index. That is where we stand today, as the big five of Microsoft, Apple, Amazon, Alphabet, and Facebook comprise 20% of the S&P 500. From a historical standpoint this is a very rare situation.  So far this year, these Big 5 companies' stock performance looks like this:

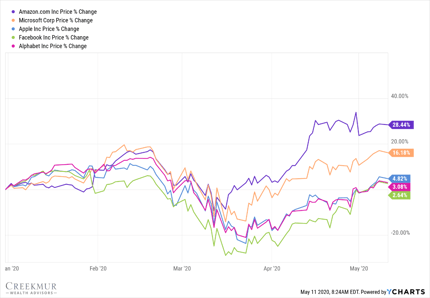

So far this year, these Big 5 companies' stock performance looks like this:

Clearly Microsoft & Amazon are performing very well. Both have benefited from the current stay at home economy, as compared to the other three companies. However, taken as a whole – these companies have significantly outperformed the S&P 500 and have been largely responsible for pulling the index back towards positive territory.

Since 20% of the S&P 500 is made up of so few companies, the hardest hit sectors of the U.S. economy have not had a big impact on the index performance. For example, so far this year the Energy sector of the S&P 500 have a YTD return of -35.43%. However, the Energy sector is only 2.70% of the S&P 500 – so the overall impact on the index is minimal. This is a great reminder of how quickly a company's fortune can change: as recently as 2014 Exxon was the second largest company in the world. Today it is the 27th largest company in the S&P 500 and risks being passed by Chevron as the largest energy company in the S&P 500 if their current trajectory continues.

Now for the million-dollar question – how does this really impact your portfolio? While returns of the S&P 500 and your portfolio can look great when the big five companies' stocks are soaring, if you are heavily invested in those positions you may be opening yourself up to significant potential for loss if those big five companies run into trouble. I would encourage you to determine if your portfolio is over-allocated to a company or sector in light of your personal risk tolerance and time horizon for each account.

If you need assistance our team at Creekmur Wealth Advisors can provide the tools and knowledge to help keep your portfolios appropriately diversified. Do not hesitate to ask for a hand.

Question of the week: How much cash should I keep in my emergency fund, and what should I do with this extra cash?

A topic as simple as how much cash you keep in your savings account could have a big impact on your overall net worth. We often find that our clients become paralyzed when making decisions around how to allocate funds due to fears such as potential market drops and loss of income. To address those fears, here are some rules of thumb to use when allocating savings:

- Keep 3 – 6 Months of Expenses In Cash Savings

There is some flexibility in this, but you should always have cash on hand to help cover for unexpected emergencies or potential loss of income. For myself I have about 4 months of cash on hand – I don’t own a house, my expenses are fairly low, and my primary objective is to invest funds for future goals like buying a house or retirement. Some of my clients who are approaching retirement may require having 6+ months on hand to help them navigate the transition into retirement with maximum peace of mind. Take the time to think through how this rule applies to your situation.

- Use a High-Interest Savings Account for Cash Savings

Most traditional savings account are earning pennies on the dollar with the national average for interest rate in a savings accounts around 0.09%. To help your savings account keep better pace with inflation we recommend that our clients utilize a High-Interest Savings account such as the one offered by Ally Bank.

If you have more than the recommended 6 months savings on hand, here are a few financial planning items to consider:

- Do You Have The Correct Life Insurance Coverage?

This topic has become a major factor in our financial planning process. Most individuals that come into our office are under insured and unintentionally putting their families at risk of financial hardship. Although no one likes to think about it, the greatest and most responsible gift you can give your family is to purchase a life insurance policy that correctly insures your life and cares for your family’s financial needs should the worst happen. To learn more about life insurance download our e-book.

- Have You Maxed Out Your IRA or Roth IRA accounts?

Every individual under the age of 50 with earned income or a spouse who has earned income can contribute up to $6000 per year to an IRA or Roth IRA account. Every individual over the age of 50 with earned income or a spouse who has earned income can contribute up to $7000 per year to an IRA or Roth IRA account. This is a simple, tax efficient way to get cash on hand working for your future use in retirement.

- What Goals Do You Have On The Horizon?

Every financial plan is made up of unique goals and timelines. When you have extra cash in your Emergency Fund it's a good time to review your goals and time frame for accomplishing them. If the amount you have allocated for a specific goal isn't accumulating at the correct pace, it might be time to put your excess savings to use with the correct asset allocation for the goal in question. For example – I have been saving for a new home purchase in the next few years. Since our time frame is less than five years, we are not taking a great deal of risk with our savings for this goal, however we would like to have a better return on our funds than what we would receive in a savings account. So, we have allocated some extra cash to a Moderate Conservative risk investment allocation in our brokerage account. We have no desire to lose a considerable chunk of these funds if the market were to decrease, however we recognize that with the correct risk tolerance we can achieve a better return than the savings account in question and will be able to move closer to our goal in less time!

The above principles can be applied broadly to every unique situation to help you make the best decision possible and solidify your financial plan. This is a great time to review your personal plan and prioritize the best way to put your cash on hand to work for you.

Creekmur Wealth Advisors may be reached at 866-358-4441 or Info@Creekmurwealth.com.

Citations.

1 - https://www.investopedia.com/ask/answers/05/sp500calculation.asp