Today we will cover the last type of annuity: fixed index annuities. This type of annuity guarantees no loss of principal due to the market fluctuations and interest earned is linked to the performance of an external market index. Fixed index annuities first appeared in the 1990’s as an alternative to traditional fixed annuities.

How Fixed Index Annuities Work

Typically, a fixed index annuity offers a choice of indexes on which to base your interest credits. You may also have the option to receive fixed interest-that is, a set interest amount credited regardless of the performance of the index.

While the annuity is not actually participating in the market, when the index performs well, the interest is credited up to a predetermined amount, based on that performance. However, when the index performs poorly, nothing happens-the annuity’s value doesn’t go down an there is no loss of principal or previously accumulated interest.

Most fixed index annuities have components that help determine how much interest can be credited in a given year. The most common are:

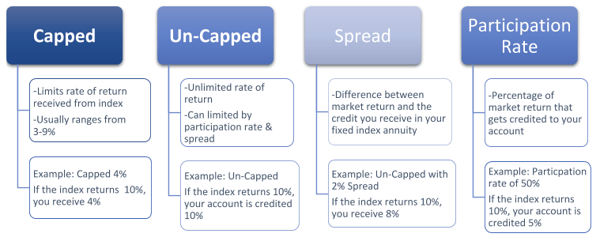

Capped fixed index annuities have a limit on a maximum interest rate (or cap) that the contract can earn in a specified period. Uncapped fixed index annuities don’t put a limit on your interest earnings. Rather, they allow you to capture 100% of the index’s return, but they can be limited by a participation rate or spread.

Spreads are the difference between the actual index return and what you receive in your fixed index annuity. For example, if the insurance company’s annuity contract has a 3% spread and the index returns 10%, then you would receive an interest credit of 7%. Participation rates are the percentage of interest earned that the insurance company will pass on to your annuity contract.

Benefits of a Fixed Index Annuity

Fixed index annuities can be beneficial because they have the potential for growth while providing a level of guarantees. The insurance company protects your account from a loss in the market, removing the risk of losing your principal due to marker declines.

As with all annuities, the earnings accumulated are tax free. Additionally, this annuity can fulfill an income need, while providing growth potential as well. Outpacing inflation is possible, as long as your participation rate is relatively high, and your spread is relatively low.

Another benefit of a fixed index annuity is the lower fees. The only fees that are taken from a fixed index annuity are riders, whether that be an income rider, death benefit rider, long-term care rider, etc. This helps keep your account growing, since less money is being taken from your annuity to pay for fees.

Additional Considerations of a Fixed Index Annuity

With those aspects in mind, it’s important to highlight the limit of growth potential. Unlike a variable annuity, fixed index annuities can limit to your interest credits, whether that’s a direct cap or a limit via spread or participation rate. However, there may be some select fixed index annuities that allow you to track un-capped indices.

Also, annuities contain certain costs and because they are long-term contracts, there may be charges or penalties for taking money out early. If you are under the age of 59 ½, there may also be a 10 percent federal tax penalty.

Because of guarantees and protections provided by annuities are backed by the financial strength and claims-paying ability of the issuing insurance company, buyers may wish to do some research about the insurance company that is providing the annuity before making a purchase. To inquire about the insurance company, you may contact the insurance company or your state insurance department. Be sure to choose your insurance company wisely when purchasing an annuity contract.

Right Fit for a Fixed Index Annuity

Fixed index annuities are beneficial for those who want to protect their principal investment while receiving some growth. People who want to outpace inflation but also mitigate risk of loss can benefit from a fixed index annuity.

Wrapping Up Fixed Index Annuities

Fixed index annuities combine many of the positive features of variable annuities and fixed annuities. Although they are one of the most complex type of annuity, they have many benefits that can help you prepare for or continue retirement or other long-term needs. The lack of market risk does limit potential growth, but safety is important in a fixed index annuity. Always be sure to dive deep into your annuity contract and understand exactly what it contains.

Feel free to contact Creekmur Wealth Advisors with any fixed index annuity questions!

This is provided for informational purposes only and is not intended to provide specific tax advice or serve as the basis for any financial decisions. Be sure to speak with qualified professionals before making any decisions about your personal situation. Please note that the information included herein from third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed.

Securities and advisory services offered only by duly registered individuals through Madison Avenue Securities, LLC (MAS), member of FINRA/SIPC. Investment advisory services offered only by duly registered individuals through AE Wealth Management, LLC (AEWM), a Registered Investment Adviser. MAS and Creekmur Wealth Advisors are not affiliated entities. AEWM and Creekmur Wealth Advisors are not affiliated entities. 00189678