Today, we will dive into a deeper analysis of fixed annuities. These annuities were the original type of annuity and were used for centuries for funding wars, retirement funds, and taking care of soldier’s families while they were gone. Currently, they are still used by many as a form of fixed retirement income. Let’s get into the details!

How Fixed Annuities Work

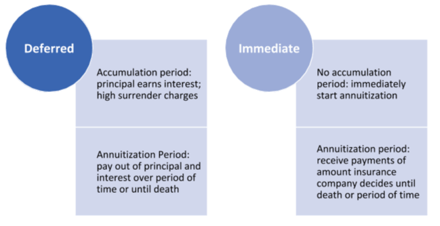

With fixed annuities, you contribute a lump sum or series of payments, known as the premium, to an insurance company in exchange for the annuity contract. There are two main types of annuity contracts: Deferred and Immediate.

Deferred annuities have a more typical annuity timeline, where there’s both an accumulation period and an annuitization period. With this type of fixed annuity, you will earn interest on your principal -- getting both your principal and interest back, minus any withdrawals, in the shape of monthly or annual payments during the annuitization phase. These annuities can sometimes be helpful for those who are still a few years from retirement, or the recently widowed.

Immediate annuities have a different timeline, where there’s no accumulation period. Instead, you immediately start receiving monthly or annual payments. Something to note here is that you do receive interest in an immediate annuity, but it may be lower than in a deferred annuity. Additionally, you are primarily getting your principal back with these monthly payments. The payouts you receive are taxed at ordinary income tax rates.

It’s important to note that once you decide to receive payments for life, the transaction is irreversible, and you no longer have access in a lump sum. And, when you die, any remaining contract value that could have been left to your heirs is forfeited to the insurance company.

Both types of fixed annuities have their place in planning for retirement. It is important to speak with a Creekmur Wealth Advisor to decide if either are the right fit for your situation.

Benefits of a Fixed Annuity

Fixed annuities are generally more secure than other types of annuities in that they have no market risk—you’re given a set, fixed interest rate. Additionally, you are fixed your principal back, minus any withdrawals, in addition to that promised interest rate through those monthly or annual payments.

With deferred fixed annuities, the interest you earn is tax-deferred, meaning you don’t pay taxes until you withdraw payments. Withdrawals or surrenders prior to age 59 ½ may be subject to a 10 percent federal additional tax. These annuities may fill the need for fixed income and allow you to have some tax-deferred gains while meeting that need.

Additional Considerations of a Fixed Annuity

A risk with fixed annuities, particularly those with long terms, is spending power loss. Unlike Social Security, fixed annuities have no cost of living adjustments, and therefore inflation may beat your annuity’s fixed interest rate. This causes a loss in spending power. Of course, this is only a possibility, but an important one to note when considering a fixed annuity.

Also, annuities contain costs and because they are long-term contracts, there may be charges or penalties for taking the money out early.

Because the guarantees and protections provided by annuities are backed by the financial strength and claims-paying ability of the issuing company, buyers may wish to do some research about the insurance company that is providing the annuity before making a purchase.

To inquire about the insurance company, you may contact the insurance company or your state insurance department. Be sure to choose your insurance company wisely when purchasing an annuity contract.

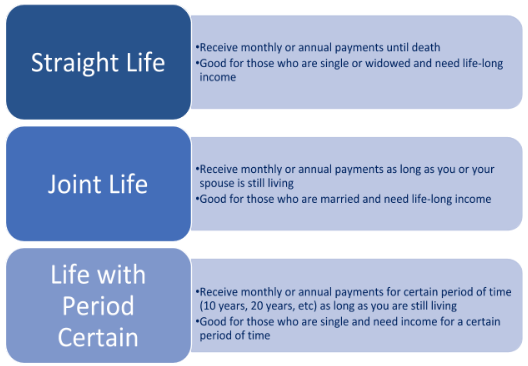

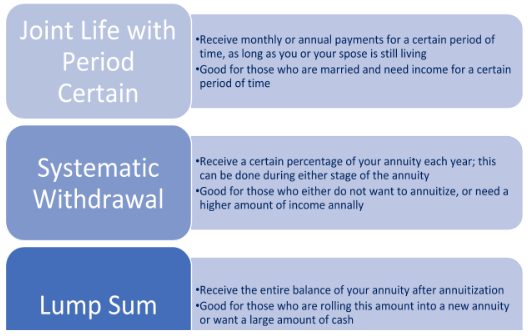

Payout Options

There are many options to consider when deciding how your payments are structured. Some factors to consider are: How much do you need each month? How long do you need this income to last? Do you have a spouse you may leave behind?

While considering these factors, let’s take a look at the various payout options:

There are many options for payouts. Talk with a Creekmur Wealth advisor about your preferences when considering a fixed annuity for your True Wealth goals.

The Right Fit for Fixed Annuities

Before deciding on an annuity, it’s important to look at whether or not a fixed annuity is the right fit for you. Fixed annuities may be good for older clients heading towards or have already entered the retirement stage. Risk-averse clients may prefer fixed annuities.

Some wealthy clients might use fixed annuities to grow their principal tax deferred. Those who have already maxed out their other tax-deferred retirement funds like their 401(k)s and their IRAs may benefit from a fixed annuity. Using income riders can potentially expand the scope of usefulness in a fixed annuity as well, although they typically require an additional fee.

Wrapping Up Fixed Annuities

Fixed annuities have many benefits, as well as disadvantages to consider. They can be the right fit for many, but not all. It’s important to consider your options when looking at what type of fixed annuity you want, as well as which payment option you will choose. It’s important to understand the features of your annuity contract to make sure everything is the way you want it, and that you are confident in your investment.

Feel free to contact Creekmur Wealth Advisors with any questions about fixed annuities.

This is provided for informational purposes only and is not intended to provide specific tax advice or serve as the basis for any financial decisions. Be sure to speak with qualified professionals before making any decisions about your personal situation. Please note that the information included herein from third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed.

Securities and advisory services offered only by duly registered individuals through Madison Avenue Securities, LLC (MAS), member of FINRA/SIPC. Investment advisory services offered only by duly registered individuals through AE Wealth Management, LLC (AEWM), a Registered Investment Adviser. MAS and Creekmur Wealth Advisors are not affiliated entities. AEWM and Creekmur Wealth Advisors are not affiliated entities. 00189678