Welcome back to our series about annuities! This time, we will be diving a little deeper into the basics of annuities. We will look at how annuities work and some important terms to concentrate on when thinking about an annuity or examining an annuity contract. First, let’s take a look at the history of annuities. They’ve been around for a very long time and have evolved over the many years.

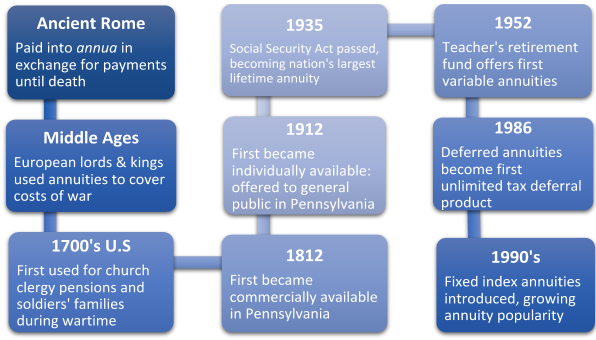

The History of Annuities

How do Annuities Work?

Today, annuities are a type of insurance product used for retirement or other long-term needs. They are tax deferred, meaning no taxes are paid on the interest that is credited to the contract. Withdrawals are subject to ordinary income tax and, if taken prior to 59 ½, may be subject to a 10 percent federal additional tax. To buy an annuity contract, you pay a lump sum or a periodic contribution, known as the premium, to the insurance who is offering the annuity contract. Once your annuity contract has been issued, you are now in the accumulation stage. During the accumulation stage, your annuity earns interest, growing the value of your contract over time.

Once you want to start taking out payments from the annuity, you will transition into the annuitization, or income, stage. In this stage, your contract no longer earns interest, rather, you receive monthly or annual payments out of the annuity until death or the end of a term contract. In exchange for lifetime income, you lose access to the funds in the annuity.

For many of our annuity clients, we keep their annuity contracts in the accumulation stage, and if income is needed, withdraw the maximum amount allowed without surrender fees, or we utilize an income rider. By doing this, we maintain some liquidity and growth potential while helping to meet our clients’ income needs.

Types of Annuities

There are three main types of annuities: fixed, variable, and fixed index annuities. The next three handouts will be on each of these in detail, so today we’ll just get down the basics. Understanding these different types is important in deciding whether or not an annuity is the right choice for your True Wealth goals.

- Fixed

- As it sounds, this annuity guarantees a fixed interest rate for a predetermined number of years throughout the growth stage of the annuity contract.

- Variable

- This annuity is invested into financial securities that may provide a higher rate of return or may result in a loss—with a negative rate of return.

- Fixed Index

- Fixed index annuities guarantee no loss of principal, and due to the market fluctuations and interest is linked to the performance of an external market index up to a certain percentage of the overall index’s return.

Annuity Fees

One of the downsides to an annuity is the cost of fees. Most annuities charge 2-5% of your premium in annual fees. The fees charged can have a negative impact on the overall investment performance. However, if the fee being paid results in an investment solution that meets an individual’s needs, then it can be in the client’s best interest to pay it. Let’s break down exactly what you’re paying for in these fees, if applicable:

Surrender Charge

Occurs when the free withdrawal limit has been exceeded for the year; can be fairly high.

Surrender charge periods range in length from 1-20 years.

Rider Fees

Add-ons available on many annuity contracts in the form of living or death benefit or an income rider.

Additional fees that are typically included in a variable annuity include:

Insurance Fees

Mortality and Expense portion: covers insurance guarantee of return of contract value at time of contract owner’s death

Administrative portion: covers selling and organizational expenses of contract

Investment Management Fees

The investments involved in the annuity contract require more expensive management, resulting in a management fee

Annuity Riders

Annuities come with a basic contract, usually that performs like what you read above. Without riders, your annuity has a standard death benefit which is typically a return of premium or the accumulated value of the contract, and you have no guaranteed rate of interest on your income as you withdraw in the annuitization phase. This is where annuity riders come in: living benefits and death benefits. Living benefits are more commonly referred to as income riders, because that’s what they provide—at a cost of course. Income riders are guaranteed growth in your annuity through the annuitization phase.

Death benefits on the other hand provide a beneficiary with your annuity balance or an increased death benefit, whether that is a spouse, child, or even a charity. The costs of riders usually range from .5% to 2% of your annuity contract’s value, billed on an annual basis. Riders may not be available in all states or on all annuity products.

Surrendering an Annuity

With annuities, there is a term involved in every contract called surrender. This usually refers to the “surrender charge period,” which is a 1-20 year time period in which you are limited in how much money you can withdraw from your annuity. The longer you have an annuity, the lower the fees to withdraw your money, after you’ve reached the surrender charge free withdrawal limit.

The term “surrender” can also refer to surrendering your annuity, meaning you close the contract and take out all of your money. If you are still in your surrender charge period, you will lose a certain percentage of your contract value. Additionally, depending on the tax qualification and the interest earnings of the annuity contract, you may have to pay taxes in some capacity. Withdrawal or surrenders prior to age 59 ½ may be subject to a 10 percent federal additional tax.

Wrapping Up the Basics

The most important thing to remember is that annuities are complex financial products that require understanding. It is important that you are educated on the features of your annuity contract. Remember, annuities are not the right product for everyone. Talk with a Creekmur Wealth Advisor about your True Wealth goals today to see if annuities are an appropriate option for you.

Annuity guarantees and protections are backed by the financial strength and claims paying ability of the issuing insurer.

This is provided for informational purposes only and is not intended to serve as the basis for any financial decisions. Be sure to speak with qualified professionals before making any decisions about your personal situation. Please note that the information included herein from third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed.

Securities and advisory services offered only by duly registered individuals through Madison Avenue Securities, LLC (MAS), member of FINRA/SIPC. Investment advisory services offered only by duly registered individuals through AE Wealth Management, LLC (AEWM), a Registered Investment Adviser. MAS and Creekmur Wealth Advisors are not affiliated entities. AEWM and Creekmur Wealth Advisors are not affiliated entities. 00189678